With the cryptocurrency market recovering from its harsh winter of last year, crypto hedge funds seem to be gaining popularity again, which is why we took a look at a report release by PwC and Elwood about the way the top 100 hedge funds are run, the solutions they offer, the magnitude of assets they handle and how that translates into a raise in the number of users.

To clarify, hedge funds are generally investment funds that pool capital from investors (usually institutions) and invest in various assets, implementing risk management criteria and different techniques for portfolio management, in order to increase said capital over time. Crypto hedge funds act in a similar way, but they trade in cryptocurrency exchanges, which generates additional benefits while also dealing with the increased risk of volatility.

PwC, a network of advisory firms with presence in 158 countries and a crypto-focused team of more than 150 professionals, worked with Elwood, an investment firm specialized in digital assets, to perform a worldwide analysis of what crypto hedge funds look like at the moment, comparing them to their state in 2017 and 2018.

Size of Market

One of the first topics that needs to be covered is how the crypto hedge funds are holding up after last year’s rough moments, starting with the main strategies they use. 19% of these funds are described as “fundamental” (long-term and slow trading techniques, hold more liquid cryptos), while 37% are “quantitative” (fast-paced trading, oriented towards market-making and arbitrage) and 44% are “discretionary” (hybrid approach). From that we can say that more hedge funds are open to offering different trading strategies to properly fulfill their clients’ needs.

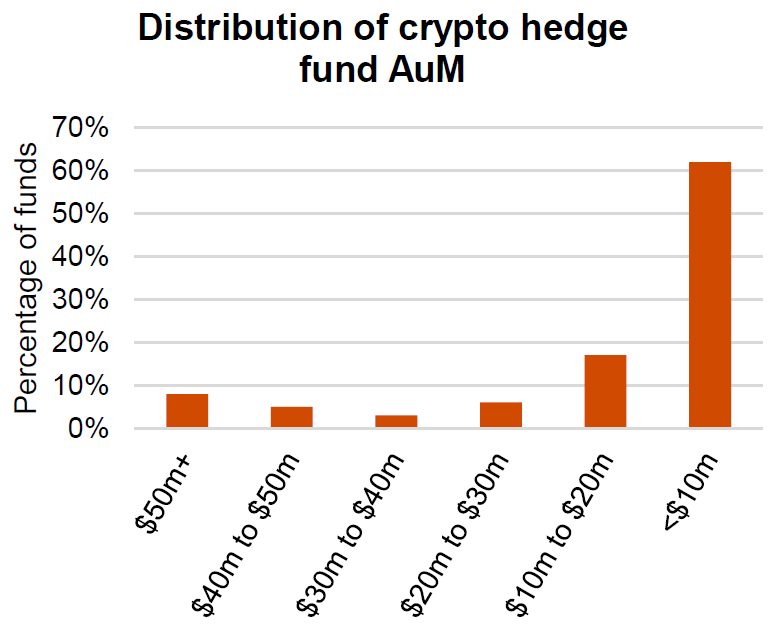

What’s interesting to look at is how assets are distributed among these hedge funds: collectively, the analyzed hedge funds represent an average of $21.9 million. However, the median of this list is $4.3 million, which means that most of the assets are being kept in a few funds while many of the funds hold way smaller amounts.

It’s also important to notice that the average value of the assets in hedge funds at launch is $3.6 million, with a median of $1.2 million, which means that the business of crypto hedge funds is currently generating income, implying they survived the low stage of the market.

And besides generating income for their users, hedge funds also need to generate enough revenue to sustain themselves, and they do so by charging fees. The average management fee among all the studied hedge funds was of 1.72%, with discretionary funds having the highest average at 1.76% and quantitative having the lowest at 1.57%.

However, that represents a very small amount of money when you consider the value of the assets they manage, which is why most hedge funds are looking for new ways of generating revenue. Some take the route of charging performance fees that round 23% to compensate these losses (quantitative funds charge the highest performance fee at 26.8% while their management fee is the lowest), but in a market that became more reluctant after how most coins fell last year. Other strategies include working as advisors for early-stage projects or do some trading by themselves and market-making.

Strategies and Results

The main strategic difference between the different kinds of crypto hedge funds is whether they allow their users to take short positions, which implies placing quick, small trading orders with the main intention of buyback. 86% of quantitative funds allow this, along with 80% of discretionary funds and none of the fundamental funds that were examined.

Another strategy that was analyzed was if the use of leverage was permitted, and this shows an opposite distribution to short positions. Only 36% of the reviewed funds allow the use of leverage, meaning that they are a bit more cautious in this aspect.

In terms of results, as one would expect, the returns were negative. Due to the big drops on cryptocurrency, adding up to a 72% drop in Bitcoin, crypto hedge funds had a hard time trying to generate any revenues, getting to a median return of -46%. Fundamental funds managed to end up slightly better than discretionary funds, with medians of -53% and -63% respectively, due to their strategy of investing in ICOs and exiting in early stages.

Non-Investment Data

The second part of the report gives an insight into the administrative aspects of crypto hedge funds, analyzing items like governance, custody, team size and experience and others.

Out of the crypto hedge funds that were reviewed, the average team size was 7.5 (with a median of 6), with a total average experience of 24 years (median of 20). An interesting point is that only 7% of the teams stated they use third-party research for their operation, which may occur due to the low number of thorough crypto-related research that currently exists, so the teams rather operate on their own data.

In terms of governance, only 25% of the analyzed funds have independent directors, with the other 75% having corporate directors to compensate with the lack of directors with enough expertise in terms of cryptocurrency. On the other hand, there is a more balanced distribution when talking about the use of internal or external custodians (48-52, respectively), which caters to the needs of some customers who value the distribution of funds as a safety measure.

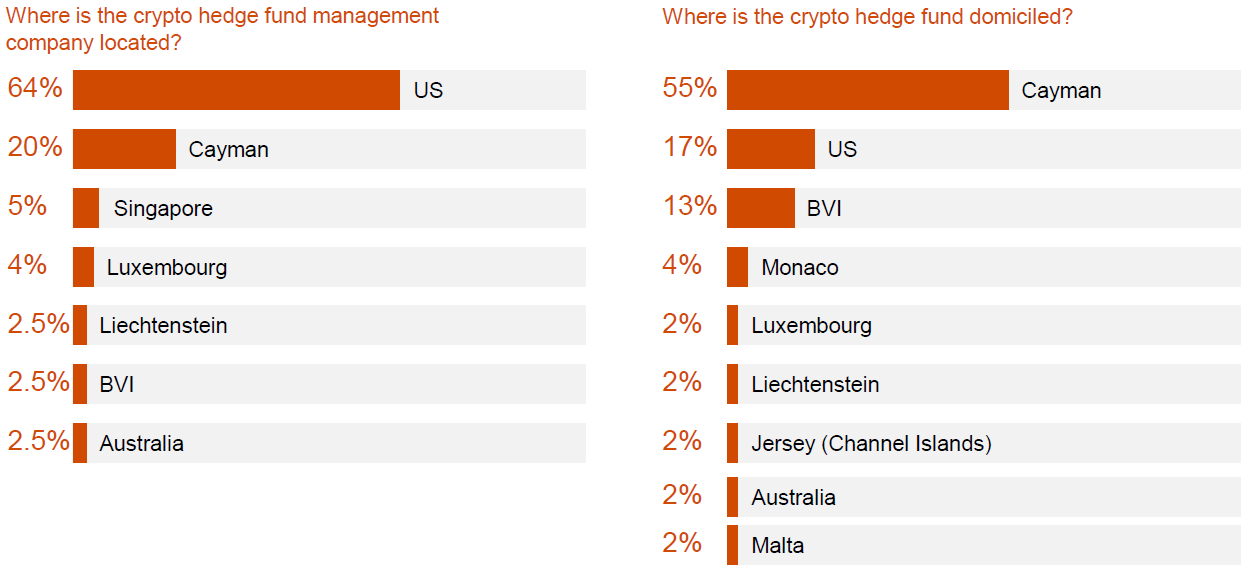

When looking at the legal and regulatory aspects, the location of the company’s offices and the domicile of the fund are very relevant, as they are useful to determine which countries give the most liberties for the management of such funds. 64% of companies are managed from the US, while 55% of funds are domiciled in the Cayman Islands, much like traditional hedge funds. They then advice that customers should be aware of this information, as some may not agree with that sorts of practices, even when domiciling the fund in a different location might be beneficial in terms of legal repercussions.

Overall, PwC and Elwood made an extensive report with a significantly large data pool, which can be of use for future customers or interested investors to take a well-informed decision about using the services of crypto hedge funds. Of course, it’s also important to note that the market is currently in a very different place than where it was last year, so it would be wise to compare this results with another studies that may be published later this year.